Emergency Fund: How Much Should You Actually Save?

Building an emergency fund is one of the most supportive things you can do for your financial wellness, but figuring out how much emergency savings you actually need can feel confusing. While traditional advice says to save three to six months of expenses, the truth is that your ideal emergency fund depends on your lifestyle, responsibilities, income stability, and personal financial goals. In this guide, we’re diving into emergency savings tips and financial security planning strategies that help you create a safety net that actually fits your life.

Before we get into numbers, I think it’s important to acknowledge something that doesn’t get talked about enough when it comes to emergency savings: most people aren’t avoiding saving because they’re irresponsible. They’re avoiding it because life feels expensive, unpredictable, and honestly… overwhelming sometimes.

When you’re juggling bills, trying to enjoy your life, paying off debt, supporting family, or simply recovering from financial stress, building an emergency fund can feel like this giant impossible task sitting in the background of your mind. And then on top of that, you hear conflicting advice everywhere about how much you’re “supposed” to save.

Three months? Six months? A whole year?

The truth is, emergency funds are deeply personal. What feels financially safe for one person may feel completely insufficient for another. That’s why I don’t believe in treating emergency savings like a one-size-fits-all formula.

Your emergency fund should support your real life — your responsibilities, your income, your lifestyle, your mental well-being, and even your capacity for uncertainty. Because at the end of the day, financial wellness isn’t just about surviving emergencies. It’s about creating a sense of safety within yourself knowing you can handle them when they happen.

Emergency Funds Aren’t One-Size-Fits-All

An emergency fund is one of the most important foundations of financial security. But many people still wonder how much emergency savings they really need. In this guide, you’ll learn emergency savings tips and financial security planning strategies to help you prepare for unexpected expenses.

Life’s unpredictability can wreak havoc on even the best financial plans. From surprise car repairs to sudden job losses, having an emergency fund is a cornerstone of sound financial wellness. Yet, despite its importance, many people still feel behind when it comes to saving. Research from FP Canada found that a large percentage of Canadians feel financially stressed regularly, and many don’t have enough savings to comfortably cover emergencies.

And honestly, I get it.

Saving for emergencies can feel difficult when you’re already trying to balance rent or mortgage payments, groceries, debt repayment, investing, and just… living life. Sometimes it can feel like every dollar already has a purpose before it even lands in your bank account.

But this is exactly why emergency savings matter so much.

An emergency fund isn’t just about preparing for worst-case scenarios. It’s about creating breathing room. It’s about giving yourself options. It’s about knowing that when life inevitably surprises you, you don’t have to immediately spiral into panic, shame, or debt.

The traditional advice of saving three to six months of expenses is a good starting point, but real life is often more nuanced than that. A more holistic approach to financial planning considers your lifestyle, responsibilities, income consistency, mental well-being, and long-term goals.

Because financial wellness is never just numbers on a spreadsheet. It’s also about how safe, supported, and empowered you feel in your day-to-day life.

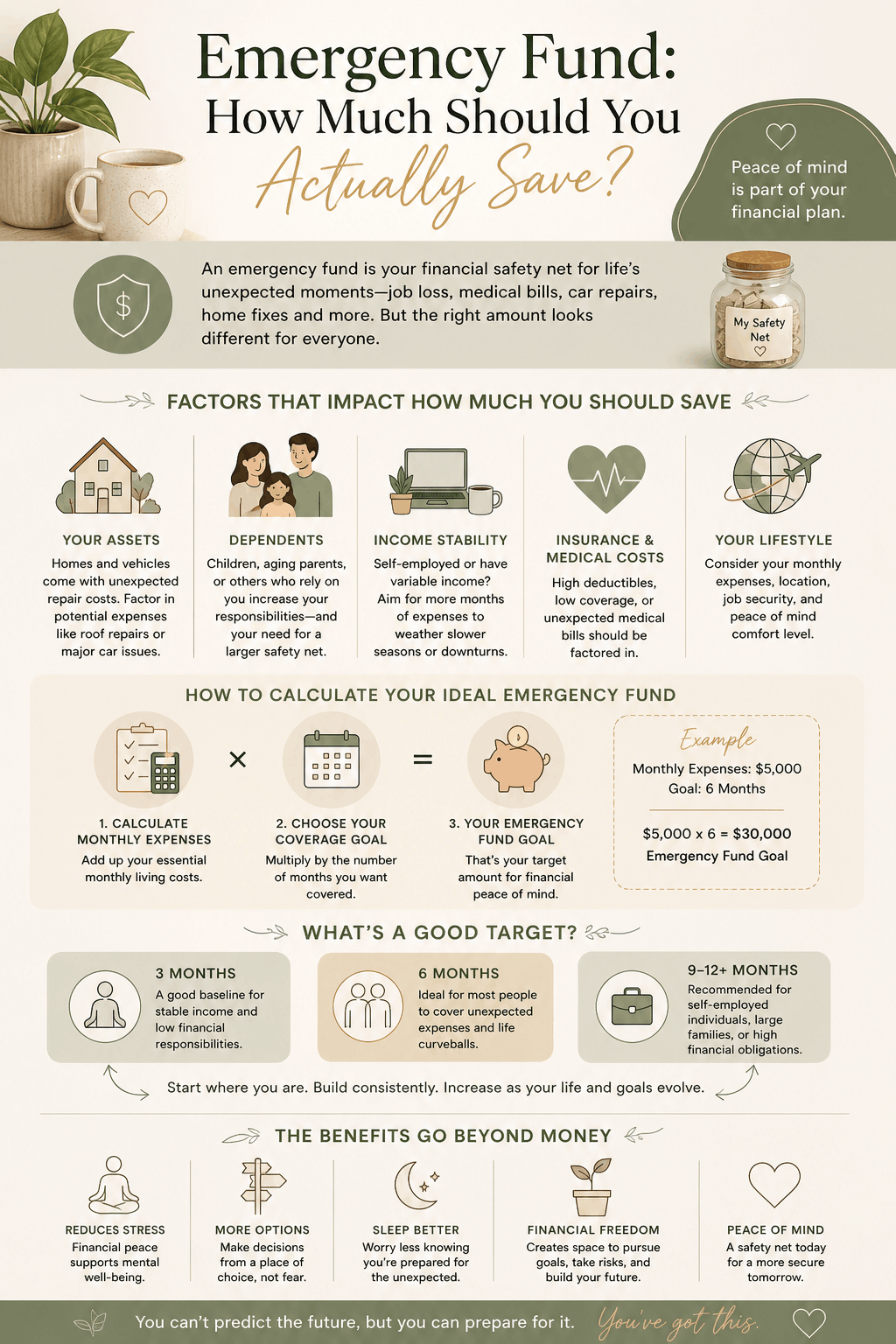

Assessing Your Assets: A Key Step in Financial Planning

Your assets, particularly high-maintenance ones like a home or vehicle, should absolutely influence the size of your emergency fund.

Homeownership can come with beautiful milestones, but also expensive surprises. Roof repairs, plumbing issues, broken appliances, flooding, electrical problems… things happen. And they usually happen at the least convenient time possible.

If a major home repair could realistically cost you $8,000–$15,000, your emergency savings should reflect that possibility. Planning ahead for these moments helps prevent relying heavily on credit cards or loans when emergencies arise.

The same goes for vehicles.

Cars are often essential for work, errands, caregiving responsibilities, and everyday life, especially if you don’t live in a walkable city. Whether it’s a transmission repair, replacing tires, or an unexpected accident deductible, vehicle expenses can add up quickly.

This is something I break down further in The Psychology of Money style conversations around preparedness and long-term thinking: financial security often comes from expecting life to be imperfect instead of hoping emergencies never happen.

Taking inventory of your assets and their potential repair costs is one of the most supportive things you can do when building a realistic emergency fund.

Young female child holding baby male sibling or family member from behind.

Dependents Change Your Financial Needs

If you have dependents, your emergency savings should grow alongside your responsibilities.

Children bring so much joy into life, but they also come with unpredictable costs. Medical expenses, childcare, school-related expenses, activities, groceries, clothing — the list evolves constantly as they grow.

And if you’re caring for aging parents or financially supporting family members, that creates another layer of responsibility that deserves consideration in your financial planning.

One thing I think we don’t talk about enough is how emotional it can feel when someone depends on you financially. There’s a deep desire to protect the people we love, and having emergency savings can help ease some of that emotional pressure.

Research from the American Psychological Association has consistently shown that financial stress can significantly impact mental health and relationships. Having savings in place doesn’t eliminate life’s difficulties, but it can create more stability during uncertain moments.

Your emergency fund isn’t just protecting your bank account. It’s protecting your nervous system too.

Why Self-Employed Individuals Need Larger Emergency Funds

If you’re self-employed, freelance, or running a business, your emergency savings strategy likely needs to look different from someone earning a stable salaried income.

Income fluctuations are normal in entrepreneurship. Some months are abundant, while others can feel slower or uncertain. And during those slower seasons, emergency savings become incredibly important.

The pandemic highlighted this reality for so many people. Entire industries shifted overnight, contracts disappeared, businesses had to pivot, and many individuals realized how vulnerable inconsistent income can feel without savings in place.

For self-employed individuals, saving six to nine months of expenses — or even more — can provide a stronger sense of financial stability.

And honestly, having a larger emergency fund can also create more creativity and freedom within your work. When you’re not operating from survival mode constantly, it becomes easier to make aligned decisions instead of fear-based ones.

If financial inconsistency is something you’re currently navigating, I dive deeper into building supportive financial habits in “How to Stop Living Paycheck to Paycheck Without Feeling Restricted.” Sometimes financial security starts less with making more money immediately and more with creating stronger systems around the money you already have.

Insurance and Medical Costs Matter More Than We Think

One thing many people underestimate when building an emergency fund is healthcare-related expenses.

Even with insurance or healthcare coverage, unexpected medical costs can happen quickly. Dental work, prescriptions, therapy, physiotherapy, emergency travel, specialist appointments, and other health-related expenses can create financial strain unexpectedly.

A holistic financial wellness plan accounts for these possibilities instead of ignoring them.

This doesn’t mean living in fear or constantly expecting something bad to happen. It simply means acknowledging that life is unpredictable sometimes, and creating support systems ahead of time.

And there’s something deeply calming about knowing you’ve prepared for yourself in advance.

How to Calculate Your Ideal Emergency Fund

Creating an emergency fund starts with understanding your monthly baseline expenses.

This includes:

Housing costs

Utilities

Groceries

Insurance

Transportation

Minimum debt payments

Childcare

Healthcare expenses

Essential subscriptions or bills

From there, multiply your monthly expenses by the number of months you want covered.

For example:

Monthly expenses: $5,000

Six-month emergency fund: $30,000

But remember — this number is personal.

Someone with stable dual-income employment and no dependents may feel comfortable with three months of savings. Meanwhile, a self-employed parent with a mortgage may feel safer with nine to twelve months saved.

There isn’t one perfect number that applies to everyone.

The goal is creating enough financial cushion that you feel supported during unexpected situations.

Start Small if You Need To

I think one of the biggest mistakes people make with emergency savings is believing they need to have the full amount immediately.

You don’t.

If saving several months of expenses feels overwhelming right now, start with your first $500. Then your first $1,000. Then one month of expenses.

Financial wellness is built gradually.

And honestly, small consistent habits matter more than occasional perfection. Research from behavioral finance studies continues to show that consistency and automation often outperform extreme short-term financial efforts that are difficult to sustain long-term.

This is also why I created the Wealth Well Tracker — because building wealth usually happens through supportive systems and intentional habits, not overnight transformations.

Further Reading

Continue Building Your Financial Security

If you’re currently working on feeling more financially grounded and supported, these posts may help you go even deeper.

The Emotional Benefits of Emergency Savings

One of the most underrated parts of having an emergency fund is the emotional relief it creates.

There’s a different kind of peace that comes from knowing you can handle unexpected situations without immediately falling apart financially.

An emergency fund can help reduce financial anxiety, improve decision-making, and create more flexibility in your life. It can allow you to leave unhealthy work environments, take career risks thoughtfully, rest when needed, or simply breathe a little easier knowing you have support behind you.

And I think that’s really what financial wellness is about.

Not just accumulating money endlessly, but creating a life where you feel safe, supported, and empowered.

Emergency savings are one part of that foundation.

Not because life will always go according to plan — but because sometimes it won’t.

And you deserve to feel prepared either way.

Free Resource To Start With

If building an emergency fund still feels overwhelming or confusing, my Wealth Well Tracker can help you organize your finances in a way that feels supportive instead of restrictive. It’s designed to help you build better money habits, track your savings goals, and create more clarity around your financial wellness journey.

Affiliate Recommendation

One tool that can genuinely help when building emergency savings is Wealthsimple, especially if you want a separate high-interest savings account to automate your emergency fund contributions. Keeping your savings slightly separated from your everyday spending account can make it easier to stay consistent and avoid dipping into it impulsively. Sign up now to get a $25 referral bonus.

Frequently Asked Questions

How much should I keep in an emergency fund?

Most financial experts recommend saving three to six months of living expenses, but your ideal emergency fund depends on your income stability, dependents, assets, and lifestyle.

What counts as an emergency expense?

Emergency expenses include unexpected situations like medical bills, car repairs, job loss, urgent home repairs, or emergency travel.

Should I pay off debt or build an emergency fund first?

In many cases, it’s helpful to build a small emergency fund first while continuing minimum debt payments. This helps prevent relying on credit cards when unexpected expenses arise.

Where should I keep my emergency fund?

A high-interest savings account is often the best place for emergency savings because it keeps your money accessible while still earning some interest.

How long does it take to build an emergency fund?

The timeline varies depending on your income, expenses, and savings capacity. Building emergency savings gradually over time is completely normal.

Do self-employed people need larger emergency funds?

Yes. Self-employed individuals often benefit from saving six to nine months of expenses because income can fluctuate more significantly.

〰️ WORK WITH ME

↳ my coaching services https://bit.ly/3ZAs0NZ

↴ additional resources and perks:

→ Download my free ebook on mastering your money mindset https://bit.ly/3fAfj33 💵

→ Download my free Wealth Tracker - https://bit.ly/48H8Rxj 🧮

→ Invest in stocks with Wealthsimple https://bit.ly/3PJYscp 📈

→ Invest in crypto and receive $25 USD https://bit.ly/3TxD4dr 🪙

→ Invest like the rich in art and receive a $200 bonus (USD only) https://bit.ly/3Popuqh 🖼️

→ Sign up for my bi-weekly newsletters https://bit.ly/466g09H 📨

〰️ CONTACT ME

✉️ hello@morganblackman.com