Mortgage Calculator

Let’s estimate what your future mortgage payment could look like.

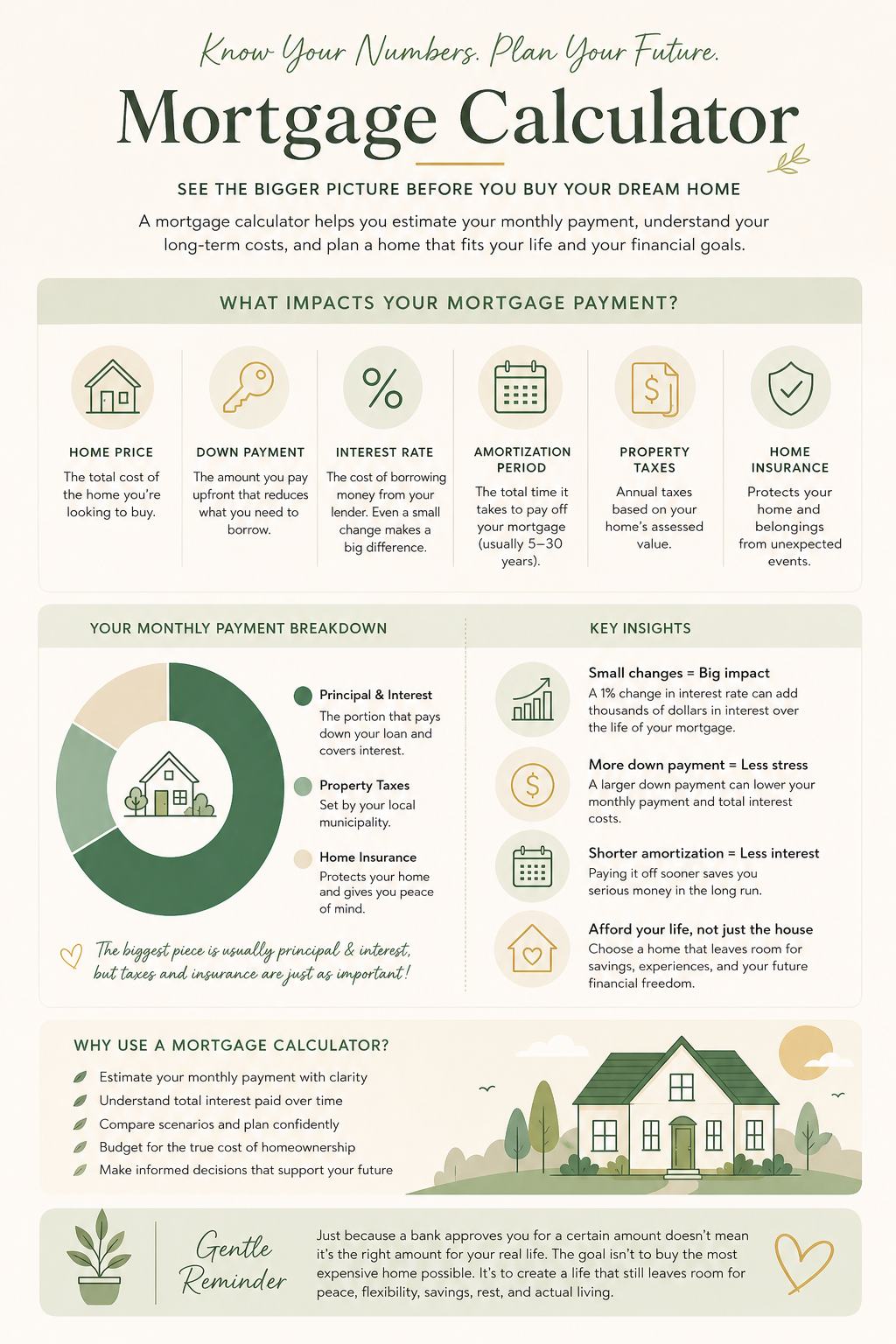

Use this mortgage calculator to explore your estimated monthly payment based on your home price, down payment, interest rate, amortization period, property taxes, and insurance. This tool gives you clarity before you make one of the biggest financial decisions of your life.

$0

$0

$0

$0

$0

Disclaimer: This mortgage calculator is for educational and illustrative purposes only. It does not include every possible cost of homeownership, such as condo fees, utilities, closing costs, maintenance, mortgage insurance (PMI/CMHC), or lender-specific fees. Always speak with a qualified mortgage professional before making a final decision.

Start PlanningBuying a home is exciting, but honestly? It can also feel incredibly overwhelming when you start looking at the actual numbers.

Maybe you’re wondering how much house you can realistically afford. Maybe you’re trying to understand how interest rates impact your monthly payment. Or maybe you’re stuck somewhere between wanting your dream home and wanting financial peace at the same time.

I get it.

This mortgage calculator is designed to help you estimate your monthly mortgage payment, understand your long-term interest costs, and create more clarity around one of the biggest financial decisions you’ll ever make.

Because homeownership should feel empowering — not emotionally suffocating.

And sometimes seeing the numbers clearly is what helps everything finally feel a little more grounded.

According to the Financial Consumer Agency of Canada, mortgage payments are influenced by several factors including your home price, down payment, amortization period, and mortgage interest rate. Even small changes to interest rates or down payments can significantly impact your long-term costs over time.

Why Use a Mortgage Calculator?

A lot of people start house hunting before they actually understand what their future monthly payment may look like.

And honestly, that’s usually where stress starts creeping in.

Because once you add together mortgage payments, property taxes, insurance, utilities, maintenance, groceries, debt payments, and everyday life expenses… things can start feeling very real very quickly.

This mortgage payment calculator is designed to help you slow things down and create more clarity before making a major financial decision.

Not from a place of fear.

Not from restriction.

Not from panic.

But from a place of understanding.

You can use this calculator to estimate:

Monthly mortgage payments

Total interest paid over time

Amortization timelines

Down payment impacts

Property tax and insurance costs

Overall monthly housing expenses

And honestly? Sometimes the most powerful thing about using a mortgage affordability calculator is simply realizing what feels sustainable for your life.

Not what the bank says you technically qualify for.

Not what social media says you “should” buy.

But what actually allows you to feel financially safe while still living your life.

How To Use This Mortgage Calculator

This calculator helps estimate your future mortgage payment based on several key factors involved in homeownership.

The first thing you’ll enter is your home purchase price. This is the total cost of the property you’re considering buying.

Then you’ll enter your down payment amount. Your down payment directly impacts how much you’ll need to borrow, which also affects your monthly mortgage payment and long-term interest costs. In Canada, down payments under 20% may also require mortgage default insurance through CMHC or another provider, which can increase total borrowing costs over time.

Next, you’ll enter your mortgage interest rate. And honestly, this is usually the part people underestimate the most.

Even small differences in interest rates can dramatically impact how much interest you pay over the life of your mortgage. This is why many people use a mortgage interest calculator before buying a home — it helps you understand the true long-term cost of borrowing, not just the monthly payment itself.

You’ll also enter your amortization period, which is the total amount of time it will take to fully pay off your mortgage. Longer amortization periods usually lower monthly payments but increase total interest costs over time.

Finally, you can include estimated property taxes and home insurance costs to create a more realistic picture of your total monthly housing expenses.

Because your mortgage payment is rarely the only cost of owning a home.

Understanding Mortgage Interest

One of the hardest parts about buying a home right now is how expensive interest has become.

And honestly? A lot of people focus so heavily on the home price itself that they forget to calculate how much interest may cost over 20 or 30 years.

That’s why using a mortgage payment calculator matters so much.

For example, even a 1% increase in mortgage rates can raise monthly payments significantly and add tens of thousands of dollars in additional interest over the life of a mortgage.

Which sounds dramatic… because it kind of is.

But this isn’t meant to scare you.

It’s meant to help you make informed decisions before signing onto a payment that may affect your financial wellbeing for decades.

This is also why buying a home that feels emotionally and financially sustainable matters so much more than simply stretching yourself to the absolute maximum budget possible.

Your future self deserves breathing room too.

The Emotional Side of Buying a Home

Can we talk about this for a second?

Buying a home is emotional.

For some people, it represents safety.

Stability.

Freedom.

Success.

A fresh start.

A lifelong dream.

And for others, it can also bring up fear, pressure, comparison, scarcity, or anxiety around money.

Especially in today’s housing market.

A lot of people feel pressure to “buy now before it’s too late,” while also wondering whether they’ll ever truly feel financially ready.

And honestly, both feelings can exist at the same time.

This is why I think it’s so important to approach homeownership from both a practical and emotional perspective. Because buying a home should not come at the expense of your mental health, your relationships, your retirement goals, or your ability to actually enjoy your life.

A mortgage should support your future — not emotionally consume it.

If financial anxiety has been taking over your thoughts lately, I dive deeper into this in “Financial Anxiety: How to Stop Money Stress From Controlling Your Life.” And if you’re trying to build a healthier relationship with money overall, “How to Build a Healthy Relationship With Money” may also help support you through this season.

What Impacts Your Monthly Mortgage Payment?

Several factors affect your mortgage payment, including:

Home purchase price

Down payment amount

Mortgage interest rate

Amortization period

Property taxes

Home insurance

Mortgage insurance (if applicable)

And honestly, this is why two homes with the exact same purchase price can still have very different monthly costs.

Even increasing your down payment slightly may reduce monthly payments and long-term interest expenses significantly over time.

This is also why building savings before purchasing a home matters so much.

Not because you need to become “perfect” financially before buying.

But because having financial flexibility can make homeownership feel far less stressful long-term.

Continue Learning About Money & Homeownership

If you’re preparing to buy a home or improve your finances overall, these articles may help you go deeper:

Free Resource

If you’re currently preparing for homeownership, my free Wealth Well Tracker can help you organize your finances, savings goals, spending habits, and debt repayment in a way that feels supportive instead of overwhelming.

It’s designed to help you create more financial clarity without turning money into something stressful or obsessive.

Frequently Asked Questions

What is a mortgage calculator?

A mortgage calculator estimates your monthly mortgage payment based on your home price, down payment, interest rate, amortization period, property taxes, and insurance costs.

How much mortgage can I afford?

How much mortgage you can afford depends on your income, debt, down payment, interest rate, and overall monthly expenses.

How does mortgage interest work?

Mortgage interest is the cost of borrowing money from a lender. A portion of each payment goes toward interest while the rest reduces your loan balance.

Does a larger down payment lower mortgage payments?

Yes. A larger down payment reduces the amount you need to borrow, which may lower monthly mortgage payments and total interest costs over time.

What is an amortization period?

An amortization period is the total amount of time it takes to fully pay off your mortgage through regular payments.

Should I buy a home at the top of my budget?

Not necessarily. Many people benefit from choosing a home that allows room for savings, emergencies, retirement contributions, and everyday living expenses.

What additional costs should I budget for when buying a home?

Additional homeownership costs may include property taxes, insurance, maintenance, utilities, closing costs, and mortgage insurance.

Book A Clarity Call 🤙🏾

So now you see the vision… but do you have the plan? If you’re ready to turn projections into progress, let’s hash it out together. Book your complimentary clarity call now, and we’ll design your roadmap to financial freedom.