Debt Payoff Calculator

Find Out When You’ll Be Debt-Free

Use this free debt payoff calculator to estimate how long it will take to pay off your balance and how much interest you’ll pay. Get a clear timeline to financial freedom.

–

$0

Why Use a Credit Card Payoff Calculator?

A lot of people know they want to become debt-free, but they don’t actually know what that looks like in real numbers. And honestly, when we avoid the numbers altogether, debt usually starts feeling even heavier than it actually is.

Maybe you’ve found yourself making payments every month but your balance barely moves. Maybe you keep telling yourself you’ll “deal with it later,” but later keeps turning into another stressful month of interest charges and financial anxiety. Or maybe you feel embarrassed about how much debt you have and avoid checking your accounts entirely because it instantly overwhelms your nervous system.

I get it. Truly.

Debt can hold so much emotional weight. It’s rarely just about the numbers themselves. It can represent survival, burnout, under-earning, financial trauma, stress, or simply trying to keep your head above water during expensive seasons of life. A lot of people carry shame around debt while ignoring the context that created it in the first place.

But avoiding debt usually creates more anxiety, not less.

This credit card payoff calculator is designed to help you estimate your debt-free timeline, understand how interest impacts your balance, and create a more sustainable debt repayment plan without relying on shame or restriction to motivate yourself. Because honestly, sometimes clarity itself becomes the first form of relief.

According to Equifax Canada, consumer debt levels continue to rise across the country as households navigate increasing costs of living and high-interest borrowing. So if paying off debt feels harder right now, you’re not imagining it. Financial pressure is very real right now. But having a clearer plan can help you feel less emotionally trapped inside of it.

How To Use This Credit Card Debt Payoff Calculator

This debt repayment planner is designed to help you create more clarity around your finances instead of carrying everything mentally all the time.

You can use it for:

Credit card debt

Student loans

Personal loans

Car loans

Consolidation loans

Lines of credit

Multiple debt balances

Here’s what to enter.

Your Current Debt Balance

This is the total amount you currently owe.

And please hear me when I say this:

Your debt balance is not your identity.

Whether it’s $2,000 or $50,000, your debt does not determine your intelligence, your discipline, or your worthiness.

We’re simply getting honest about the numbers so you can move forward with more intention instead of fear.

Your Interest Rate

This is the annual interest rate attached to your debt.

Interest is essentially the cost of borrowing money, and high-interest debt can make repayment feel painfully slow because a portion of your payment goes toward interest before it touches the actual balance.

A lot of people search for an interest credit card calculator because they’re trying to understand why their debt barely changes despite making regular payments.

And honestly? That confusion makes complete sense.

When interest compounds month after month, balances can grow much faster than most people expect.

This is why calculating credit card payoff timelines can feel so eye-opening. It helps you understand how much interest may cost over time and how different payment amounts may change your debt-free date.

Your Monthly Payment

This is how much you plan to pay toward your debt each month.

And please don’t fall into the trap of thinking progress only counts if you can make huge aggressive payments.

Consistency matters more than intensity.

A realistic debt repayment plan you can sustain usually works far better than an extreme plan that burns you out after six weeks.

Even small extra payments can make a bigger difference than you think over time.

This is something I break down further in “4 Debt Payoff Strategies That Help You Become Debt Free Faster” because sustainable repayment matters just as much as the math sometimes.

Your Repayment Timeline

This helps estimate how long it may take to become debt-free based on your current payment strategy.

Sometimes the biggest shift isn’t even the numbers themselves.

It’s realizing your debt actually has an ending point.

Because when debt feels permanent, motivation disappears.

But when you can see progress mapped out clearly, repayment starts feeling more possible.

How Credit Card Interest Works

One of the hardest parts about debt is realizing how much interest changes the total cost over time.

Especially with high-interest credit cards.

For example, if you carry a balance month after month, interest continues accumulating on whatever remains unpaid. This is why credit card debt can sometimes feel impossible to escape even when you’re consistently making payments.

The Financial Consumer Agency of Canada explains that making only minimum payments on revolving debt can significantly increase both repayment time and the total amount of interest paid.

And honestly? That realization can feel frustrating.

But it can also become empowering.

Because once you understand how interest works, you can start making financial decisions that actually support you instead of keeping you stuck.

Things like:

Increasing payments slightly

Consolidating higher-interest debt

Refinancing when appropriate

Prioritizing higher-interest balances first

Creating a more intentional spending plan

Small shifts really do compound over time.

And if spending patterns are part of what’s making repayment difficult, I talk more about this in “Conscious Spending: How to Spend Money Without Guilt” and “Mindful Spending: How to Align Your Spending With Your Values.”

Why Minimum Payments Keep You Stuck

Can we talk about this for a second?

Minimum payments are designed to keep accounts active — not necessarily to help people become debt-free quickly.

Which means if you’re only making minimum payments, a huge portion of your payment may be going toward interest instead of the principal balance itself.

This is why calculating credit card minimum payment timelines can feel honestly shocking sometimes.

You realize how long repayment may actually take without a larger strategy in place.

And listen — this is not about shaming yourself.

A lot of people make minimum payments because they genuinely cannot afford more right now.

That’s real.

But even increasing payments slightly when possible can sometimes save you thousands in long-term interest costs.

This is where a debt repayment planner becomes really helpful because it allows you to test different scenarios without emotionally spiraling every time you open your banking app.

✨ Gentle Reminder: minimum payments are designed to keep your account active — not necessarily help you become debt-free quickly. When you only pay the minimum, a large portion of your payment may go toward interest instead of your actual balance. Even increasing your payment slightly each month can help reduce long-term interest costs and shorten your repayment timeline more than you might think. The goal isn’t perfection. It’s creating enough momentum that your money starts working for you instead of against you.

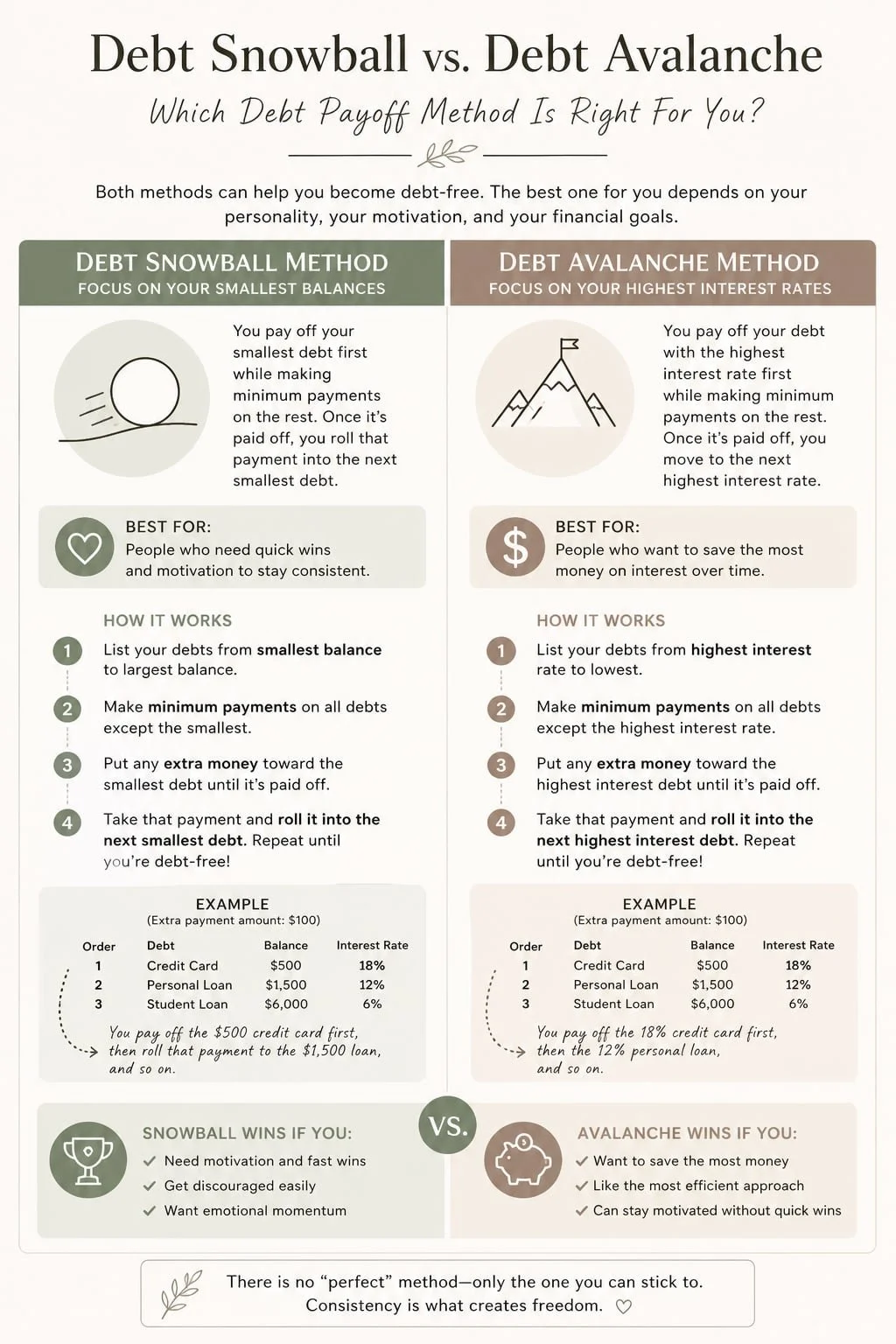

Debt Snowball vs Debt Avalanche

There’s no single “perfect” way to pay off debt.

But two of the most common repayment methods are the debt snowball and debt avalanche strategies.

Debt Snowball

With the debt snowball method, you pay off your smallest debt first while continuing minimum payments on everything else.

This creates emotional momentum through quick wins.

And honestly, emotional momentum matters more than people realize.

Sometimes seeing one debt disappear completely is what helps people finally believe change is possible.

Debt Avalanche

With the debt avalanche method, you focus on paying off the highest-interest debt first.

Mathematically, this usually saves more money over time because it reduces interest costs faster.

Neither method is wrong.

The best debt repayment plan is usually the one your nervous system can actually sustain consistently.

Because personal finance is emotional too.

I dive deeper into this in “How to Pay Off Debt Fast Using 4 Simple Strategies.”

The Emotional Side of Debt

Debt is rarely just about numbers on a screen. Most of the time, it’s connected to something much deeper. Survival. Burnout. Under-earning. Stress. Family patterns. Financial trauma. Trying to keep up. Coping during difficult seasons of life. Not having enough support. A lot of people carry intense shame around debt while completely ignoring the context that created it in the first place.

And honestly, shame usually doesn’t help people change.

Support does. Structure does. Self-awareness does. Compassion absolutely does.

Research from the American Psychological Association continues to show strong links between financial stress, anxiety, sleep disruption, and emotional burnout. So if debt has been affecting your mental health lately, you are not being dramatic. Financial stress impacts your entire body, which is why debt can feel emotionally exhausting even when you’re “doing everything right.”

This is also why building a debt payoff plan that still leaves room for joy, rest, and actual living matters so much. We are not trying to become debt-free by emotionally destroying ourselves in the process. A sustainable debt repayment plan should support your wellbeing too, not just your bank account.

If financial anxiety has been consuming your thoughts lately, “Financial Anxiety: How to Stop Money Stress From Controlling Your Life” may help you feel a little less alone in it. And if you’re trying to rebuild trust with money overall, I talk more about this in “How to Build a Healthy Relationship With Money.”

Ways To Pay Off Debt Faster

You do not need to become a completely different person overnight to make progress with debt repayment.

Start small.

Start realistic.

Start sustainable.

Here are a few ways to support your debt payoff journey:

Automate extra payments when possible

Put unexpected income toward high-interest debt

Reduce interest rates strategically

Create a values-based spending plan

Track progress monthly instead of obsessing daily

Increase payments gradually as income grows

Build a small emergency fund alongside repayment

Because honestly?

One of the hardest parts of paying off debt is staying consistent while life continues happening at the same time.

This is where systems matter more than motivation.

And if your budget keeps falling apart every month, “How to Fix Your Budget When It Isn’t Working” can help you create something that actually supports your real life instead of fighting against it.

Continue Learning About Debt & Money

If you’re ready to build a healthier relationship with money while paying off debt, these articles may help you go deeper:

4 Debt Payoff Strategies That Help You Become Debt Free Faster

Financial Anxiety: How to Stop Money Stress From Controlling Your Life

Free Resource

If paying off debt has been feeling overwhelming lately, my free Wealth Well Tracker can help you organize your finances in a way that feels supportive instead of restrictive.

It’s designed to help you track spending, debt, savings, and financial habits without turning your finances into something shame-filled or obsessive.

Frequently Asked Questions

What is a credit card payoff calculator?

A credit card payoff calculator estimates how long it may take to pay off debt based on your balance, interest rate, and monthly payment amount.

How does a credit card debt payoff calculator work?

A credit card debt payoff calculator uses your balance, interest rate, and repayment amount to estimate your debt-free timeline and total interest costs.

What is a debt repayment plan?

A debt repayment plan is a structured strategy for paying off debt over time using consistent monthly payments and payoff goals.

What is the fastest way to pay off credit card debt?

The fastest way to pay off credit card debt usually involves paying more than the minimum payment, reducing interest rates when possible, and using strategies like the debt avalanche or debt snowball method.

Why does my credit card balance barely go down?

High interest charges and minimum payments can cause balances to decrease very slowly over time, especially with high-interest credit cards.

What is the debt snowball method?

The debt snowball method focuses on paying off your smallest debt balances first to create momentum and motivation.

What is the debt avalanche method?

The debt avalanche method prioritizes debts with the highest interest rates first to reduce total interest costs over time.

Should I save money or pay off debt first?

This depends on your financial situation, but many people benefit from building a small emergency fund while also paying down high-interest debt.

Book A Clarity Call 🤙🏾

So now you’ve seen the vision, thanks to my handy debt calculator… but do you have the plan? If you’re ready to turn projections into progress, let’s hash it out together. Book your complimentary clarity call now, and we’ll design your roadmap toward debt-free living.