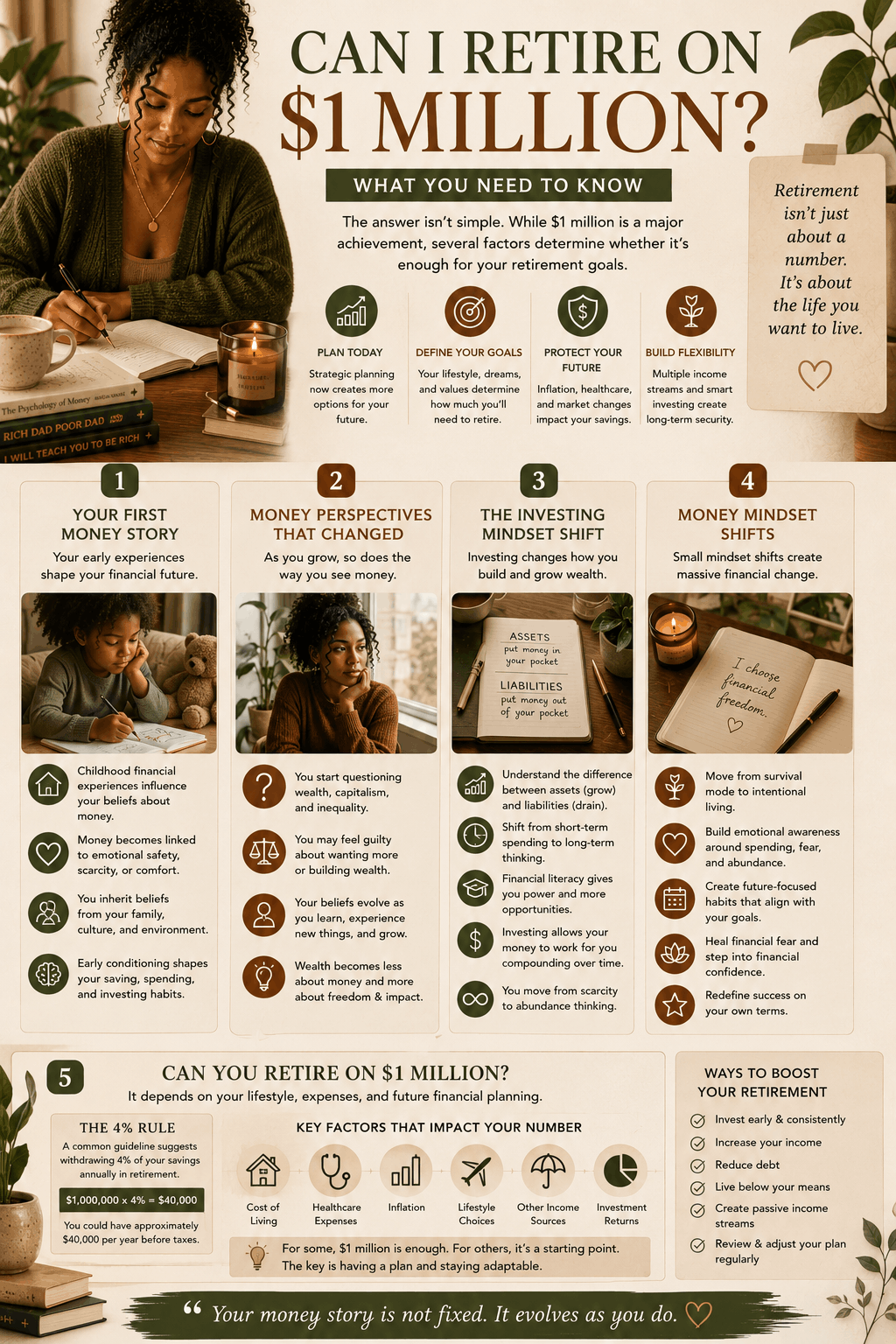

Can I Retire on $1 Million? What You Need to Know

For many people, saving one million dollars feels like the ultimate retirement milestone. But in today’s economy, the question is no longer simply how to reach that number — it’s whether that number is actually enough. In this reflective guide, Morgan explores retirement goals, inflation, healthcare costs, and future financial planning to help you understand what retiring on $1 million really looks like today.

I think one of the most interesting things about money is how certain numbers become symbolic.

For a long time, one million dollars represented ultimate financial success in people’s minds. It felt like the finish line. The number that meant you had officially “made it.” And honestly, I think many people still carry that emotional association today.

But the reality is that retirement planning has changed dramatically over the years.

Inflation has changed.

Housing costs have changed.

Healthcare costs have changed.

Life expectancy has changed.

And the overall cost of living has changed too.

So when people ask, “Can I retire on 1 million dollars?” the answer is honestly much more nuanced than a simple yes or no.

Because retirement is not only about hitting a number.

It’s about understanding the kind of life you actually want to live and whether your future financial planning realistically supports that lifestyle long term.

Why $1 Million Doesn’t Mean What It Used To

I think one of the biggest misconceptions people have around retirement is assuming one million dollars automatically guarantees financial security forever.

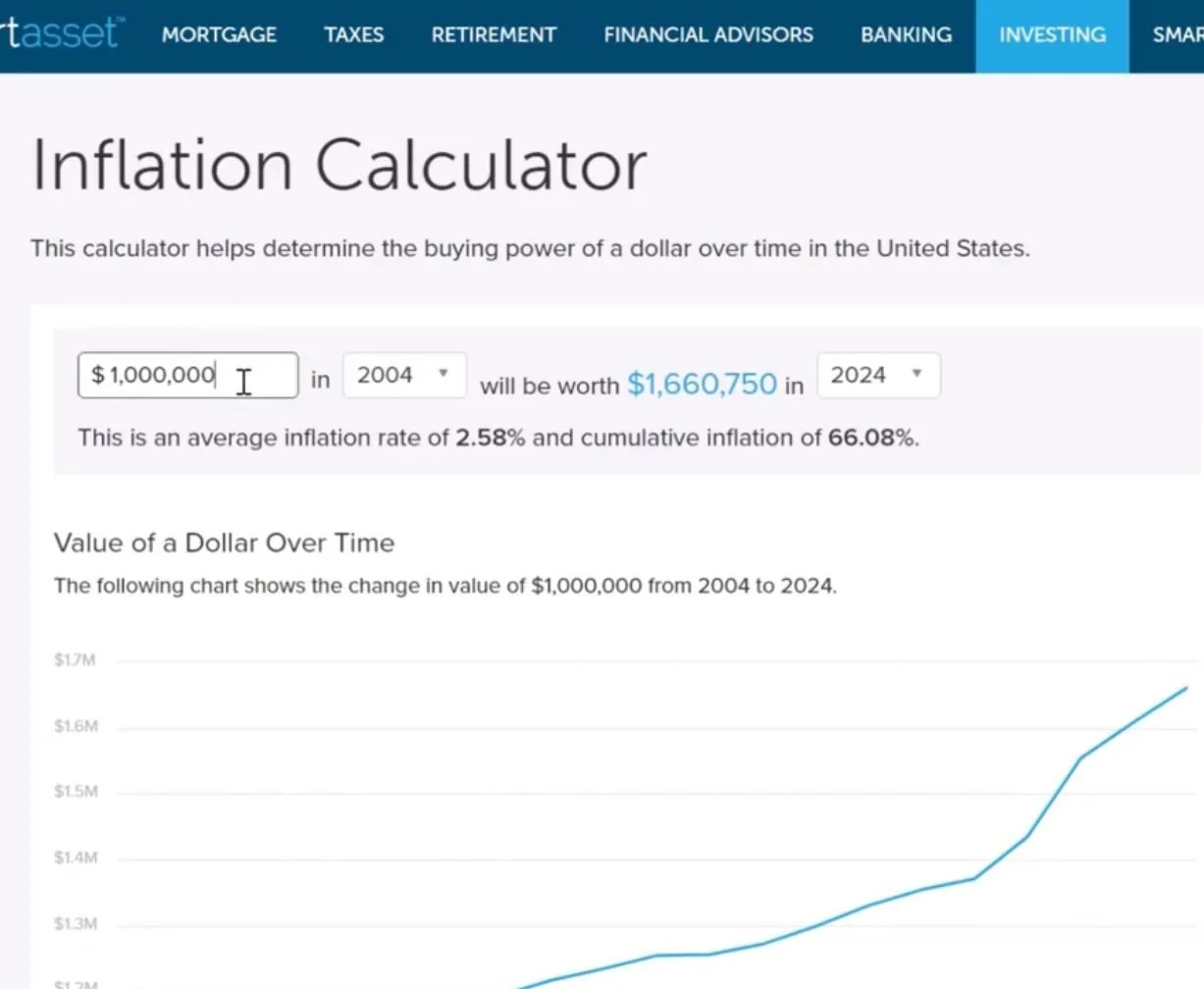

Historically, a million dollars did provide a very comfortable retirement for many people. But inflation changes purchasing power over time, which means the value of money slowly decreases as living costs rise.

And honestly, this is one of the biggest reasons future financial planning matters so much.

A million dollars today will not have the same value thirty or forty years from now. If someone plans to retire decades into the future, inflation alone could dramatically reduce how far that money stretches.

I think this is where many people begin feeling overwhelmed.

Because suddenly retirement stops feeling like a single finish line and starts feeling like an ongoing strategy.

And honestly, I think that mindset shift is important.

Financial wellness is rarely about chasing one magical number. It’s about building flexibility, adaptability, and long-term sustainability into your life over time.

Your Retirement Goals Matter More Than the Number Alone

One of the biggest factors in answering “Can I retire on 1 million?” is honestly lifestyle.

Two people with identical retirement savings can have completely different retirement outcomes depending on how they live, where they live, and what kind of life they envision for themselves.

Someone living modestly in a lower-cost area may be able to retire comfortably on one million dollars, especially if they have low debt, manageable housing expenses, and additional income streams.

Meanwhile, someone hoping for luxury travel, expensive real estate, or high monthly spending may find that same amount disappears much faster.

I think retirement goals are deeply personal.

Some people dream of traveling the world.

Others want peace, simplicity, and time with family.

Some want to retire early.

Others want part-time work even later in life because they enjoy staying active.

And honestly, I think retirement planning becomes healthier when people stop comparing themselves constantly and start defining what financial freedom personally means to them.

Because future financial planning should support your actual values — not just someone else’s idea of success.

Pssstt - click on the image to head to the Inflation Calculator website.

Understanding the 4% Rule

One of the most common retirement guidelines people reference is the 4% rule.

The idea is that retirees can withdraw approximately 4% of their retirement savings annually while still allowing investments to potentially continue growing over time.

With one million dollars invested, that would equal roughly $40,000 per year before taxes.

And honestly, whether that feels comfortable or stressful depends entirely on your lifestyle, location, debt load, and long-term expenses.

For some people, $40,000 annually may feel manageable.

For others, especially in high-cost cities, it may feel extremely limiting.

I think this is why retirement goals need to be realistic and individualized rather than purely emotional.

Because retirement planning is not only about reaching a number.

It’s about understanding the reality of your future expenses too.

Healthcare Changes Everything

I also think many people underestimate how much healthcare affects retirement planning.

Medical expenses increase significantly as people age, and longer life expectancy means retirement savings often need to last much longer than previous generations expected.

According to recent estimates, healthcare alone can cost retirees hundreds of thousands of dollars throughout retirement.

And honestly, I think healthcare costs are one of the biggest reasons future financial planning requires so much intentionality now.

Because even people who save responsibly can face enormous unexpected medical expenses later in life.

This is why retirement planning should include:

healthcare coverage

long-term care considerations

emergency savings

investment growth

inflation planning

realistic lifestyle budgeting

I think financial peace often comes less from perfection and more from preparation.

Retirement Planning Is Emotional Too

I think people often talk about retirement planning in purely mathematical terms while ignoring the emotional side completely.

But honestly, retirement is also about identity.

For many people, work has shaped their structure, routine, confidence, purpose, and sense of security for decades. The transition into retirement can feel emotionally disorienting even when someone is financially prepared.

And honestly, I think true retirement goals should include emotional wellbeing too.

What kind of life do you actually want?

What brings you fulfillment outside of work?

What relationships, hobbies, communities, or experiences matter most to you?

Because financial freedom without emotional wellbeing still feels empty eventually.

Building a More Flexible Retirement Strategy

The older I get, the more I realize future financial planning is less about predicting life perfectly and more about creating flexibility.

That might mean:

investing consistently early

building multiple income streams

downsizing later in life

delaying retirement slightly

creating passive income

reducing debt aggressively

increasing financial literacy

staying adaptable financially

And honestly, I think flexibility is one of the greatest forms of wealth.

Because life changes.

Economies change.

Priorities change.

The people who tend to navigate retirement most peacefully are often not the people who predicted everything perfectly — they’re the people who built enough financial resilience to adapt when life inevitably changed.

So, Can You Retire on $1 Million?

Honestly, maybe.

For some people, yes.

For others, probably not.

It depends on your retirement goals, your lifestyle, your health, your investments, your debt, your location, and your overall future financial planning strategy.

But I think the more important question is not only whether one million dollars is enough.

It’s whether you’re building a life that actually aligns with the future you want.

Because retirement planning is not simply about reaching a number.

It’s about creating long-term peace, stability, flexibility, and freedom.

And honestly, the earlier people begin thinking intentionally about that future, the more options they usually create for themselves later on.

Further Reading

Continue Exploring Wealth Building, Retirement & Financial Wellness

If you're building long-term wealth, planning for retirement, and trying to create more financial stability for your future, these articles may support you further.

Free Resource

If you’re trying to build long-term wealth, prepare for retirement, and create more financial freedom intentionally, download my free Money Mindset E-Book to begin strengthening your relationship with money, investing, and future financial planning.

Product Recommendation

One of the biggest things that helped me start thinking more intentionally about retirement planning was learning how to invest consistently over time instead of waiting for the “perfect” moment. I personally love Wealthsimple because it makes investing feel approachable, automated, and supportive of long-term financial growth.

FAQs

Can I retire on 1 million dollars?

Yes, it’s possible to retire on 1 million dollars depending on your lifestyle, retirement goals, healthcare expenses, location, debt, and overall future financial planning strategy. For some people, it may be enough, while others may require significantly more.

How much income does $1 million generate in retirement?

Using the common 4% withdrawal rule, $1 million could provide approximately $40,000 per year before taxes. However, actual retirement income depends on investment performance, inflation, and spending habits.

Why does inflation matter in retirement planning?

Inflation reduces purchasing power over time, meaning the same amount of money buys less in the future. This is one of the biggest reasons future financial planning and long-term investing matter when preparing for retirement.

What are the biggest retirement expenses?

Some of the largest retirement expenses include housing, healthcare, food, travel, insurance, and long-term care costs. Healthcare alone can cost retirees hundreds of thousands of dollars throughout retirement.

How can I improve my retirement planning?

Improving retirement planning often involves:

investing consistently

reducing debt

increasing retirement contributions

building multiple income streams

planning for inflation

improving financial literacy

creating realistic retirement goals