Should You Save Money or Start Investing First?

Many people struggle with the question of saving vs investing when trying to build long-term wealth and financial stability. Understanding your financial priorities, including the difference between an emergency fund vs investing, can help you make smarter money decisions with more confidence. In this guide, we’re breaking down how to decide where to focus first so you can build wealth from a place of stability instead of stress.

Should You Save Money or Start Investing First?

Many people struggle with the question of saving vs investing when building financial stability. Understanding your financial priorities, such as emergency fund vs investing, can help you decide where to focus first. In this guide, we’ll break down the key differences so you can build a smarter financial strategy.

Managing your finances is no easy feat. With the endless information online and constant financial advice coming from social media, podcasts, TikTok, and influencers, it can feel overwhelming trying to figure out what you’re actually supposed to do with your money.

And honestly? I think a lot of people feel pressure to start investing before they’re emotionally or financially ready because everyone online makes it seem urgent.

Since the pandemic especially, there’s been a massive rise in millennials and Gen Z entering the worlds of stocks, cryptocurrency, and investing. And while I genuinely love seeing younger generations becoming more financially aware and wanting to build wealth earlier, I also think many people are rushing into investing from a place of fear, scarcity, or pressure instead of education and stability.

A lot of people are trying to “catch up.”

Trying to get rich quickly.

Trying not to fall behind.

Trying to build wealth overnight because social media convinced them everyone else already has.

But sustainable wealth usually isn’t built that way.

Real investing requires patience, emotional regulation, strategy, and long-term thinking. It’s less about chasing fast money and more about creating financial freedom steadily over time.

Having invested consistently for years now, one of the biggest things I’ve learned is this: wealth building works best when your financial foundation feels safe first.

That’s why one of the most common questions I get as a holistic wealth coach is:

“Should I build my emergency fund first, or should I start investing?”

And my answer is always: it depends on your overall financial wellness.

Before investing, there are three major things I believe everyone should evaluate first.

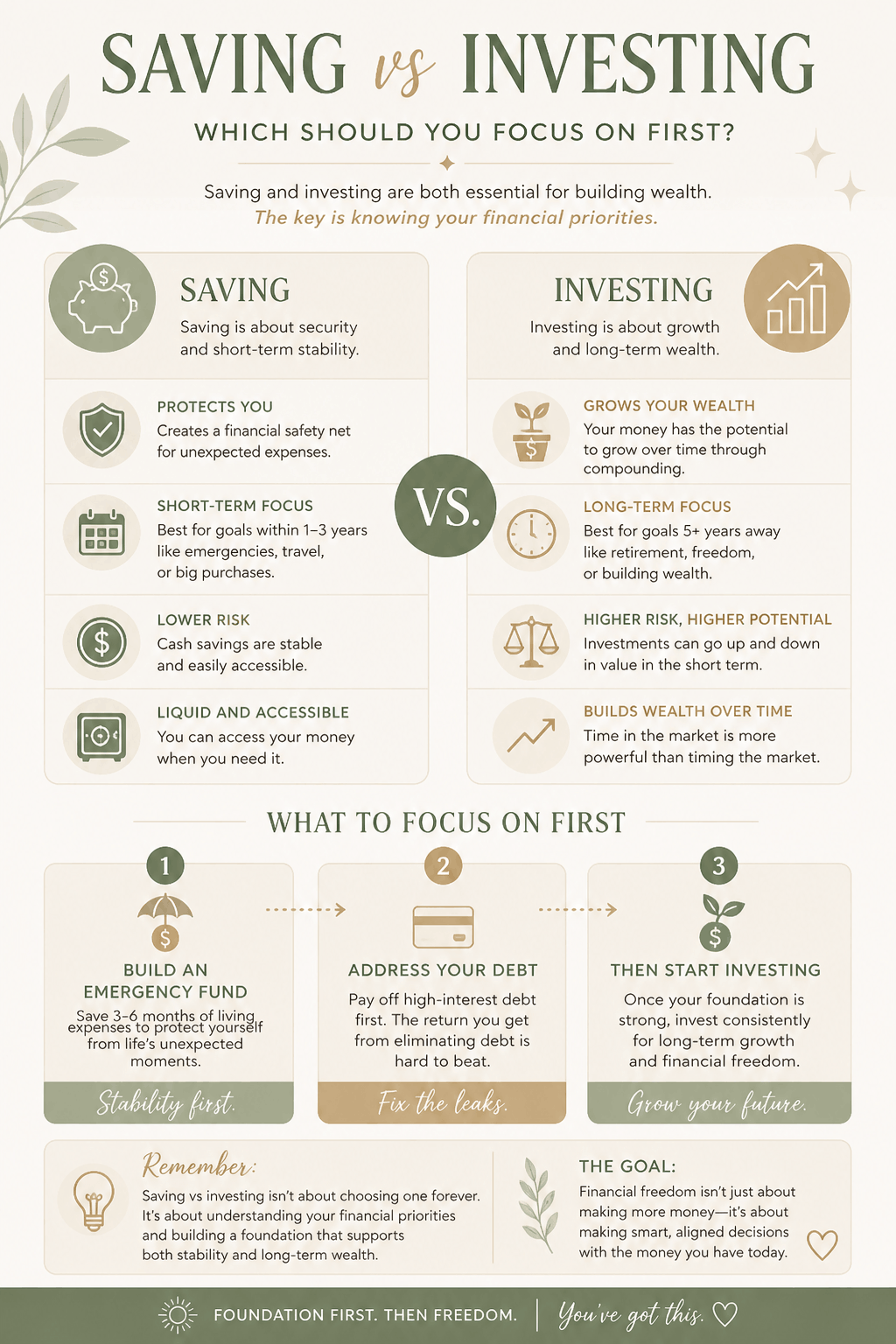

Emergency Fund vs Investing: What Should Come First?

Before you think about investing, ask yourself:

Do I have an emergency fund that could realistically support me if life suddenly changed?

Because while investing can absolutely help grow your money long-term, investing without financial stability underneath it can create more stress than freedom.

Your emergency fund is your financial safety net. It exists to protect you from unexpected situations like:

Job loss

Medical expenses

Car repairs

Emergency travel

Home repairs

Sudden life transitions

Financial experts often recommend saving three to six months of living expenses, but the right number depends on your lifestyle, responsibilities, and income consistency.

For example:

A freelancer or entrepreneur may need more savings than someone with a stable salaried job

A homeowner may need additional savings for maintenance

Someone supporting family members may need a larger cushion

Someone living at home with fewer expenses may need less

This is why I always say financial wellness should feel personal.

Research from Bankrate has consistently shown that many adults struggle to cover unexpected emergency expenses, which highlights just how important emergency savings really are. And emotionally, there’s a huge difference between investing because you feel grounded versus investing because you’re hoping investing will rescue you financially.

Your investments should not become your emergency fund.

Because if emergencies force you to sell investments too early during market downturns, you can interrupt long-term growth and potentially lose money unnecessarily.

This is something I talk more about in Emergency Fund: How Much Should You Actually Save? because emergency savings aren’t really about fear — they’re about creating stability and breathing room.

Your Debt Situation Matters Too

Before investing, it’s important to evaluate your debt honestly.

Not all debt is created equally.

High-interest debt — especially credit card debt — can quietly drain your financial progress faster than many investments can realistically grow it.

For example, the average long-term stock market return historically sits around 7–10% annually, while many credit cards charge interest rates between 20–30%.

So if your debt interest is growing faster than your investments, you may actually be losing money overall.

That’s why paying off high-interest debt is often one of the best “returns” you can give yourself financially.

Low-interest debt, however, can be more nuanced.

Student loans, mortgages, or lower-interest loans may not necessarily need to be eliminated before investing depending on your overall financial picture. Sometimes people choose to invest while slowly paying those debts down simultaneously.

The key is understanding the numbers and making intentional decisions instead of reactive ones.

This is something I dive deeper into in 4 Debt Payoff Strategies That Help You Become Debt Free Faster because debt payoff shouldn’t always come from punishment or shame. It should come from creating more freedom for your future self.

Investing Is Emotional Too

One thing I think people underestimate about investing is how emotional it can feel.

The stock market isn’t just numbers moving on a screen. It can trigger fear, comparison, greed, scarcity, and anxiety very quickly.

And if you don’t have emotional stability around money yet, investing can feel incredibly stressful.

Even experienced investors watch their portfolios fluctuate constantly. Markets rise and fall. Corrections happen. Economic downturns happen.

And during those moments, many people panic and sell prematurely because they were never emotionally prepared for volatility in the first place.

Behavioral finance research has repeatedly shown that emotional investing decisions often hurt long-term returns more than the market itself.

I’ve personally watched my own portfolio fluctuate by thousands of dollars at times. But because I trust long-term investing principles, I don’t immediately panic every time the market dips.

That emotional resilience matters.

If investing currently feels terrifying, it may not mean you’re “bad with money.” It may simply mean your financial nervous system needs more support and education first.

Sometimes practicing with demo investing accounts, reading investing books, journaling about money fears, or learning emotional regulation techniques can help build confidence gradually.

Because building wealth isn’t just financial. It’s emotional too.

Don’t Invest Money You Can’t Afford To Lose

This is one of the most important investing principles I can share.

Never invest money you immediately need access to.

Investing should come from surplus money — money that can stay invested long-term without disrupting your ability to pay bills or handle emergencies.

If losing money short-term would completely destabilize your life, that’s often a sign your foundation needs strengthening first.

And there’s no shame in that.

Honestly, social media often glorifies investing aggressively while ignoring the importance of financial safety, stability, and emotional readiness.

But sustainable wealth is rarely built from panic.

It’s built slowly.

Consistently.

Intentionally.

Why Preparation Creates Better Long-Term Wealth

Investing is powerful. It can absolutely help you build long-term wealth, financial freedom, and abundance over time.

But preparation matters.

When your emergency savings are intact, your debt is manageable, and your emotional relationship with money feels healthier, investing becomes much less stressful and far more sustainable.

That’s the real goal.

Not just building wealth externally — but creating internal financial safety too.

Because financial wellness isn’t only about growing money. It’s about feeling supported while you grow it.

Further Reading

Continue Your Wealth Building Journey

If you're currently navigating saving, debt payoff, investing, or financial anxiety, these posts may support you further.

The Three Things To Focus On Before Investing

To recap, here are three major things to prioritize before heavily focusing on investing:

Build an emergency fund with at least 3–6 months of living expenses

Pay down high-interest debt strategically

Strengthen your emotional relationship with money and investing

And remember: there’s no need to rush your financial journey.

The best wealth-building strategies are usually the ones you can sustain consistently over time.

Whatever stage you’re in right now — saving, paying off debt, learning about investing, or rebuilding financially — every step matters.

You’re not behind.

You’re building.

Free Resource to Start With

If you’re currently trying to figure out where to start financially — whether that’s saving, paying off debt, or learning how to invest — my Financial Clarity Webinar was created exactly for this stage of the journey. It’s designed to help you simplify your financial next steps so you can build wealth from a place of confidence instead of confusion.

Product Recommendation

One platform I genuinely recommend for beginner investors is Wealthsimple because it makes investing feel far more approachable and less intimidating for people who are just starting their financial journey. It’s especially helpful if you want a simple way to begin investing consistently while still prioritizing savings and long-term financial wellness.

Frequently Asked Questions

Should I save money before investing?

Yes. Building an emergency fund before investing helps create financial stability and prevents you from needing to pull money out of investments during emergencies.

How much should I save before I start investing?

Most experts recommend saving three to six months of living expenses before investing heavily, though the right amount depends on your lifestyle and financial responsibilities.

Is it better to pay off debt or invest first?

High-interest debt should usually be prioritized before investing because the interest often grows faster than investment returns.

Can I save and invest at the same time?

Yes. Many people choose to build savings while investing small amounts consistently, especially once they have emergency savings established.

Why does investing feel stressful?

Investing can feel emotional because markets fluctuate. Fear, scarcity, and uncertainty can trigger anxiety around money and long-term financial security.

What is the difference between saving and investing?

Saving focuses on protecting money for short-term needs and emergencies, while investing focuses on growing money over the long-term through assets like stocks or funds.

References

Bankrate Emergency Savings Report

https://www.bankrate.comInvestopedia — Average Stock Market Returns

https://www.investopedia.comAmerican Psychological Association — Financial Stress Research

https://www.apa.org

〰️ WORK WITH ME

↳ my coaching services https://bit.ly/3ZAs0NZ

↴ additional resources and perks:

→ Download my free ebook on mastering your money mindset https://bit.ly/3fAfj33 💵

→ Download my free Wealth Tracker - https://bit.ly/48H8Rxj 🧮

→ Invest in stocks with Wealthsimple https://bit.ly/3PJYscp 📈

→ Invest in crypto and receive $25 USD https://bit.ly/3TxD4dr 🪙

→ Invest like the rich in art and receive a $200 bonus (USD only) https://bit.ly/3Popuqh 🖼️

→ Sign up for my bi-weekly newsletters https://bit.ly/466g09H 📨

〰️ CONTACT ME

✉️ hello@morganblackman.com