The Ultimate Guide to Financial Wellbeing and Wealth

If you’re earning well but still feel stressed, uncertain, or disconnected from your money, you’re not alone. Financial wellbeing isn’t just about how much you make — it’s about your money mindset, your relationship with money, and how safe and aligned you feel managing it. In this guide, we’ll explore how to shift your money mindset, improve your financial wellness, and build a more grounded, sustainable relationship with money through both practical strategy and deeper inner work.

What Is Financial Wellbeing?

Financial wellbeing is often reduced to numbers — how much you earn, how much you save, how well you invest. And while those things matter, they only tell a small part of the story.

Because in reality, financial wellbeing is your emotional, mental, and physical relationship with money. It’s how you feel when you check your bank account, how you respond when making financial decisions, and how safe or unsafe money feels in your day-to-day life. It’s not just about having money — it’s about your experience with it.

And in many ways, it works in both directions.

The way you earn, the stability of your income, and your access to financial resources all influence your overall wellbeing. At the same time, your mental clarity, emotional state, and physical health directly impact your ability to earn, manage, and grow money. These two sides are constantly feeding into each other, which is why financial wellness is never just external or internal — it’s both.

Emotional Safety With Money

One of the most important — and often overlooked — aspects of financial wellbeing is emotional safety.

Because when you feel safe with money, your decisions change.

You’re able to think more clearly, plan more effectively, and respond instead of react. You don’t feel the same urgency or pressure behind every decision, and that alone creates better long-term outcomes.

But when that sense of safety isn’t there, a different pattern begins to emerge.

You may notice emotions like:

fear around not having enough

anxiety when thinking about the future

stress when managing or looking at money

pressure to maintain a certain lifestyle or image

And those emotions don’t just stay internal.

They shape your behavior.

There’s research in neuroscience showing that when we don’t feel safe — financially or otherwise — the body activates a stress response, shifting activity away from the prefrontal cortex (responsible for logic and planning) toward the limbic system, which is focused on survival.

Which means your financial decisions become less about strategy…

And more about relief.

How Financial Stress Impacts Decision-Making

When your body is under stress, your brain literally functions differently.

Your ability to think long-term, weigh options, and make grounded decisions becomes reduced. Instead, your system prioritizes immediate safety — even if the choices you make don’t support your future self.

This can show up in two main patterns, which many people move between without realizing:

overactive responses, where you react quickly and impulsively

underactive responses, where you avoid or shut down completely

In more activated states, this might look like:

spending money before you have it

going into debt to avoid missing out

using money to cope with stress or emotions

making decisions based on urgency rather than alignment

In more avoidant states, it can look like:

not checking your bank account

delaying financial decisions

avoiding budgeting or planning altogether

not wanting to face your financial reality

Most people don’t stay in just one of these.

They move between them.

Back and forth, depending on what feels safer in the moment.

And over time, this creates a cycle that can feel incredibly difficult to break — where moments of over-spending are followed by avoidance, and both reinforce the same underlying instability.

Eventually, that instability can start to feel familiar.

Even normal.

Why This Matters for Financial Wellness

This is why financial stress can be so limiting when it comes to building wealth.

Not because you don’t know what to do.

But because your body isn’t in a state that supports doing it.

When you’re constantly operating from stress:

your decision-making becomes reactive

your consistency becomes harder to maintain

your ability to plan long-term decreases

your relationship with money becomes strained

And over time, those patterns compound.

But when you begin to create emotional safety — even in small ways — something shifts.

Your decisions become clearer.

Your reactions soften.

Your confidence builds gradually.

And financial wellbeing starts to feel less like something you’re chasing…

And more like something you’re building from within.

If you want to go deeper into how to reduce financial stress and create a more supportive relationship with money, I expand on this in Financial Stress Management: 7 Ways to Reduce Money Stress and How to Build a Healthy Relationship With Money, where we start to move from awareness into practical change.

Understanding Your Relationship With Money

To understand your relationship with money, you have to start earlier than you think.

Most of the ways we think, feel, and behave around money aren’t fully conscious decisions. They’re patterns — shaped over time through repeated thoughts, experiences, and observations. What starts as small, seemingly insignificant ideas can slowly become the lens through which you view money entirely.

There’s research in neuroscience showing that repeated thoughts and behaviors strengthen neural pathways, meaning the more often you think something, the more automatic and “true” it begins to feel. And when it comes to money, many of those patterns were formed long before you ever had full control over your financial life.

For most people, that conditioning begins in childhood.

Whether we realize it or not, we absorb how money is handled from our environment — how our parents spoke about it, how they reacted to it, what was available or unavailable, and the emotional tone surrounding it. Over time, those experiences begin to shape not just what we believe about money, but how safe or unsafe it feels to have, manage, or grow it.

And often, without questioning it, we carry those patterns forward.

Money Beliefs: The Stories That Quietly Shape Your Reality

A belief doesn’t start as something fixed.

It starts as a thought.

Something subtle, almost unnoticeable at first.

“Money is hard to come by.”

“I never make enough.”

“I’m bad with money.”

“Rich people are greedy.”

On their own, these might feel like passing thoughts or harmless observations. But over time, when repeated enough, they begin to solidify into beliefs — and those beliefs shape how you see the world, how you make decisions, and how you respond to opportunities.

And most importantly, they shape your behavior.

Because your thoughts don’t create your reality simply because you think them once.

They create your reality through the patterns of:

emotions they trigger

decisions they influence

actions that follow

And over time, those actions become your financial life.

This is why awareness is one of the most powerful tools you can build when it comes to your financial wellbeing.

Not control.

Not perfection.

Just awareness.

A simple way to begin is to actually look at the stories you’re telling yourself about money.

You might try something like:

writing down your common thoughts about money

identifying which ones feel supportive vs limiting

gently questioning whether they’re actually true

rewriting them into something more empowering, but still believable

Because the goal isn’t to jump into unrealistic positivity.

It’s to shift into something that creates more possibility.

Childhood Money Stories: Where It Often Begins

Most of your beliefs about money don’t come from nowhere.

They come from experience.

If you grew up in an environment where money felt unstable, stressful, or scarce — where there was constant worry about bills, or where money was associated with conflict or limitation — it makes sense that you would develop a certain relationship with it.

Not consciously.

But through repetition.

You might begin to internalize ideas like:

making money is always hard

there’s never enough to go around

people with money can’t be trusted

success isn’t meant for people like me

And even if you don’t explicitly believe these things today, they can still show up in your behavior.

Because your actions will always reflect what feels true at a deeper level.

That might look like:

choosing opportunities that keep you small

undercharging or undervaluing your work

struggling to trust systems or people with money

feeling like you have to constantly prove your worth

And this is where your story becomes important.

Because your experiences are valid.

They shaped you for a reason.

I’ve seen this firsthand in my own life, especially as a Black woman navigating systems that don’t always feel designed for you to succeed in the same way. Growing up, I was often told I would have to work ten times harder to prove myself — and while that belief created resilience, it also carried pressure.

It created a sense that nothing I did would ever be enough unless I overperformed.

And that belief followed me into how I approached money, success, and worth.

Some beliefs can be both true and limiting at the same time.

And learning to hold that nuance is part of the work.

Because while we can’t always control the systems we exist within…

We can begin to shift how we respond to them.

Identity and Wealth: Who You Believe You Are With Money

At some point, your relationship with money becomes less about what you have…

And more about who you believe you are.

Society categorizes wealth in very clear ways — poor, middle income, wealthy — and with those labels come assumptions, judgments, and identities that people begin to internalize.

People who are struggling financially are often labeled as:

irresponsible

lazy

lacking discipline

While those with wealth are seen as:

successful

intelligent

hardworking

And while none of these are universally true, they still shape perception.

And perception shapes identity.

If you begin to identify as “broke,” that identity carries weight. It comes with emotions, expectations, and behaviors that reinforce it. You may start making decisions that align with that identity, not because it’s who you truly are, but because it’s what feels familiar.

But there’s an important distinction here.

Being in a financial situation is not the same as being that situation.

There’s a difference between:

being broke (fixed identity)

experiencing a period where you need more money (temporary state)

And that distinction matters more than most people realize.

Because identity can either limit you…

Or create space for change.

Your relationship with money is not just about what’s in your bank account.

It’s about how you feel in relation to it.

And those two things are not always the same.

If you want to explore this deeper, I share more of my personal journey in Your Money Story: How Money Mindset Shifts Change Your Financial Future, as well as How to Improve Your Relationship With Money (So It Finally Feels Safe) and How a Broke Mindset Around Your Insecurities Keeps You Financially Stuck, because understanding your relationship with money is where real change begins.

Money Mindset and Abundance Thinking

For a long time, I thought my money mindset was something I needed to fix.

Like if I could just think more positively, believe more in abundance, or reframe my thoughts enough… everything would eventually fall into place. And while that idea sounds appealing, it never fully landed for me in a way that felt real or sustainable.

Because no matter how much I tried to adopt a more “abundant” mindset, there were still moments where fear showed up. Moments where I felt uncertain, where I questioned my decisions, where I didn’t fully trust myself with money in the way I thought I should by that point.

And it took me time to understand that this wasn’t because I was doing something wrong.

It was because my money mindset wasn’t just built on thoughts — it was built on experiences.

Scarcity vs Abundance (What This Actually Feels Like)

We hear about scarcity and abundance all the time, but most of the time they’re explained in a way that feels overly simplified.

Scarcity isn’t just a negative mindset. It’s something your body recognizes. It’s the feeling that there isn’t enough, that you need to be careful, that something could go wrong or be taken away. It creates a tightness in your thinking and decision-making, where everything starts to feel more urgent and high-stakes than it actually is.

Abundance, on the other hand, isn’t about pretending everything is fine or ignoring reality. It’s a sense of openness. A belief — even if it’s quiet — that there are options, that things can work out, that money can flow in different ways.

What I started to notice in my own life is that I wasn’t one or the other.

I moved between both.

There were moments where I felt grounded and clear, and my decisions reflected that. And then there were moments where I felt tight, reactive, and uncertain — and my decisions reflected that too.

And that’s when something shifted for me.

Instead of asking, “Why am I thinking like this?”

I started asking, “What state am I in right now?”

Because that question created awareness without judgment.

There’s also research in behavioral economics that supports this in a really tangible way. When people experience scarcity, their focus narrows. Their ability to think long-term decreases, and they become more focused on immediate relief.

Which means scarcity doesn’t just affect how you feel.

It affects what you’re able to see.

And once I understood that, I stopped trying to force abundance — and started focusing on creating the conditions where I could actually feel safe enough to access it.

Identity Shifts: Where Financial Wellness Actually Changes

At a certain point, your money mindset stops being about your thoughts…

And starts being about your identity.

You can tell yourself that you want to feel more confident with money. That you want to build financial wellness. That you want to trust yourself more.

But if you still see yourself as someone who is:

“bad with money”

“inconsistent”

“always behind”

Your actions will continue to reflect that — even if your intentions say otherwise.

I had to face this in a very real way.

There were moments where I realized I wasn’t just struggling with money — I was identifying with being someone who struggled with money.

And that identity was shaping everything.

How I made decisions.

How much I trusted myself.

How I showed up when things felt uncertain.

The shift didn’t come from forcing confidence or trying to become someone completely different.

It came from allowing a new identity to form gradually.

One where I wasn’t perfect, but I was capable. Where I didn’t have everything figured out, but I trusted that I could learn. Where I saw myself as someone building a healthy relationship with money, instead of someone constantly failing at it.

And that felt different.

Because it was believable.

Money Manifestation & Money Energy (A Grounded Perspective)

This is also where money manifestation and money energy started to make more sense to me — not as something abstract, but as something deeply practical.

Because manifestation isn’t just about attracting money.

It’s about becoming someone who can:

receive money

hold money

make decisions with it

without it creating fear, pressure, or instability in your system.

Money energy, in a grounded sense, is simply the emotional tone of your relationship with money.

It’s how you feel when you:

earn it

spend it

save it

think about it

And over time, that emotional tone shapes your patterns.

I started to notice that when I felt more grounded, my decisions naturally shifted.

I wasn’t overthinking as much.

I wasn’t reacting as quickly.

I wasn’t trying to control everything or avoid it altogether.

There was more space between the moment and my response.

And in that space, my financial wellbeing started to feel different.

Not perfect.

But steadier.

If this is something you’re currently navigating, I go deeper into how to shift your money mindset in a way that actually feels sustainable in How to Develop an Abundance Mindset, as well as 3 Money Blocks That Stop You From Building Wealth. And if you’ve ever felt disconnected from your own inner guidance when it comes to money, Trusting Your Intuition: The Hidden Skill Behind Wealth can help you reconnect to that in a more grounded way.

Because at the end of the day, this isn’t about becoming someone new.

It’s about learning how to trust the version of you that’s already capable of doing this — even if you’re still figuring it out.

The Energetics of Money

At first glance, money seems like something purely practical.

A number in your bank account. A tool for transactions. A way to exchange goods and services so life can function more efficiently.

But when you begin to look a little deeper, money is also something more than that.

It’s relational.

It’s emotional.

And in many ways, it’s energetic.

Money as Energy (A Grounded Perspective)

When people hear the phrase “money is energy,” it can sometimes feel abstract or disconnected from reality. But in a grounded sense, it simply points to the idea that money is not neutral in how we experience it.

Because every financial decision carries meaning.

When you spend money, you’re not just completing a transaction — you’re assigning value. You’re deciding that what you’re receiving is worth what you’re giving in return. And that exchange is influenced not just by logic, but by perception, emotion, and context.

Even something as simple as buying a coffee can illustrate this.

That $10 latte isn’t just $10. It represents your time, your energy, your work. Maybe it reflects thirty minutes of effort. And in that moment, you’re deciding that the experience of that coffee — the convenience, the enjoyment, the ritual — is equal to that exchange.

And if it’s not?

Your behavior adjusts.

You opt out. You make it at home. You reassess what feels worth it.

This is where money energy becomes practical.

It’s not about the money itself.

It’s about the relationship you have with it — the meaning, intention, and awareness behind how you use it.

There’s also research in behavioral economics showing that people don’t make financial decisions purely rationally. Emotions, perceived value, and context all play a significant role in how we spend, save, and invest. Which means your financial life is shaped just as much by how you feel about money as it is by how much of it you have.

Money as a System (And Why That Matters)

Money also exists within systems that we’ve collectively created.

Before currency, humans relied on bartering — exchanging goods and services directly within their communities. If you had something I needed, and I had something you needed, we traded. Simple, local, relational.

But as societies grew, that system became harder to sustain. It required exact matches of need and value, which became increasingly impractical at scale.

So money became a shared agreement.

A way to standardize value.

A tool to make exchange more efficient.

And in many ways, that shift allowed societies to expand, organize, and grow.

But over time, something subtle changed.

Money stopped being just a tool.

And started becoming the priority.

Understanding this helped me separate money from morality.

Because money itself isn’t inherently good or bad.

It’s neutral.

But the way we structure systems around it — and the way we individually relate to it — is what shapes the outcome.

Even today, you can still see alternative forms of exchange existing in smaller, more relational spaces.

Within families.

Within communities.

Within networks built on trust and reciprocity.

People still:

share resources

exchange services

trade items like clothing, books, or skills

And not always for money.

This is something I’ve personally become deeply interested in.

I’m currently in the process of building a bartering-based foundation and app designed to support alternative exchange systems — particularly for low-income communities — as a way to create more access and flexibility outside of purely transactional systems.

Because while capitalism has created opportunity, it has also created pressure.

And I believe there’s space to reimagine how value is exchanged in ways that don’t rely solely on financial output.

If you want to explore this idea more deeply, I expand on this in Money Is Energy: A Practical Guide to Financial Flow, because understanding this alone can shift how you approach your financial wellbeing.

Money Manifestation (Without the Illusion)

Manifestation is another area where money can start to feel confusing, especially when it’s framed as something mystical or out of reach.

But in practice, it’s much more grounded than that.

It’s not about wishing for money and hoping it appears.

It’s about believing in a future that’s possible — and consistently taking action toward it.

I think of it through what I call the T.M.A Method:

Time → allowing things to unfold and compound

Mindset → believing something is possible for you

Action → consistently showing up to create it

All three matter.

Because you can’t think your way into financial wellness without action.

And you can’t take consistent action toward something you don’t believe is possible.

There’s also research in psychology showing that belief and expectation significantly influence behavior and persistence. When people believe something is achievable, they’re more likely to take action, stay consistent, and adapt when things don’t go as planned.

Which is where manifestation becomes less about magic…

And more about alignment.

In my own experience, the things that have felt easiest to “manifest” were the things I had the least resistance around. The moments where I wasn’t constantly questioning whether something would work, where I wasn’t caught in cycles of doubt or overthinking.

Because the moment doubt takes over, something shifts.

Not externally at first — but internally.

Your energy changes.

Your decisions change.

Your consistency changes.

Doubt is often just a quieter form of fear.

And while fear is natural, it can create resistance when it becomes the dominant state you’re operating from.

Not because you’re doing something wrong…

But because it changes how you show up.

This doesn’t mean you eliminate doubt completely.

It means you learn how to move forward with it — without letting it define your direction.

If you want to go deeper into this, I expand on this in Manifesting Money: How to Align Your Mindset With Wealth and 10 Manifestation Laws That Can Help You Attract Wealth, because most of the time, it’s not about doing more.

It’s about understanding what’s creating resistance in the first place.

Lifestyle Alignment and Values-Based Spending

At some point, financial wellbeing stops being about what you should be doing with your money, and starts becoming about how your money actually fits into your life.

Because you can follow every budgeting method, every piece of financial advice, every so-called “right” decision, and still feel disconnected from your money if it’s not aligned with your values. And that disconnect is subtle, but it builds over time. It shows up as regret after spending, as second-guessing decisions you’ve already made, as a quiet sense of guilt that lingers longer than it needs to.

Over time, those patterns begin to shape how you see yourself, reinforcing the idea that you’re not good with money — when in reality, what you’re experiencing is misalignment.

There’s research in behavioral psychology that shows when spending is driven more by emotion than intention, it’s far more likely to lead to regret. And that regret tends to create cycles — not clarity.

Often, it looks like:

spending → regret

regret → avoidance

avoidance → disconnection

disconnection → repeating the same patterns

And before you realize it, it’s not just about money anymore — it’s about how you feel with money.

Intentional Spending: Learning Your “Why” With Money

Intentional spending was one of the first shifts that helped me rebuild trust with my finances, and what surprised me most was that it had very little to do with restriction. It was about awareness — and more specifically, understanding the why behind my decisions.

I started slowing down just enough to ask myself questions I had never really considered before. Not in a rigid or over-analytical way, but in a way that created space between the impulse and the decision.

Questions like:

Why am I buying this?

What feeling am I trying to create?

Will this still feel good later — or just right now?

That last question changed everything, because it shifted my focus from the present moment into something more long-term and grounded.

There’s research in consumer psychology showing that even a short pause before making a purchase can significantly improve decision-making and reduce impulsive behavior. And I felt that directly — the more I slowed down, the more clarity I had.

Over time, I also started tracking my spending, not as a way to control myself, but as a way to understand myself. Because without awareness, it’s hard to know whether your money is aligned at all.

Looking back at my spending helped me notice patterns:

what genuinely supported me

what I bought out of habit or emotion

what I wouldn’t choose again

And that reflection made future decisions easier — not perfect, but more intentional.

If you want to explore this more deeply, I go further into this in Mindful Spending: How to Align Your Spending With Your Values, because this is one of the most practical ways to strengthen your financial wellbeing without overwhelming yourself.

Minimalism: Creating Space for Financial Freedom

Minimalism was one of the most unexpected shifts in my financial journey, and honestly, one of the most impactful.

I got into it through home decluttering shows and books like Marie Kondo, where the idea was simple — less, but better. At first, it felt like something purely physical. Clearing out space, organizing my environment, and creating a home that felt calmer and easier to exist in.

And that alone made a difference.

There’s research in environmental psychology showing that cluttered spaces can increase stress levels and reduce focus, which I noticed almost immediately. My space felt lighter, but more than that, my mind did too.

What I didn’t expect was how much that would affect my relationship with money.

Because once I started owning less, I started needing less. And when you need less, you naturally spend less — not from restriction, but from intention.

I became more thoughtful about what I brought into my life. If I bought something, it was because it aligned with my lifestyle, my values, or how I actually lived day to day.

Minimalism helped me step off the cycle of “more,” which often looks like:

upgrading before something is fully used

buying for identity instead of need

feeling like what you have isn’t enough

And once that pressure quieted, my spending changed naturally.

Now, my habits look completely different. I’ll typically do one intentional shopping haul in a year, and then only make occasional purchases when something is genuinely needed — like replacing a winter jacket that’s reached the end of its life.

And that doesn’t feel restrictive.

It feels freeing.

If this resonates, I go deeper into this in The Benefits of Minimalism That Improve Your Life and Finances, because this was one of the most tangible ways my financial wellness shifted in real life.

Career Alignment: The Foundation of Financial Wellness

One of the biggest influences on your financial wellbeing isn’t just how you manage money, but how you earn it.

Your work shapes your relationship with money more than most people realize. It determines not only your income, but how you feel while earning it — and that emotional experience carries into your financial decisions in ways that are often overlooked.

There’s research in occupational psychology showing that job satisfaction is closely tied to overall wellbeing, which directly impacts how people handle stress, make decisions, and plan for the future.

And yet, most of us were never taught how to find work that actually aligns with who we are.

We were taught to prioritize:

stability

status

external validation

I remember being in school and thinking success had already been defined for me — careers like doctor or lawyer being the standard. Not because they felt aligned, but because they were seen as impressive.

But over time, I started questioning that.

Whose version of success was I actually working toward?

And what would it look like to define that for myself instead?

The Japanese concept of Ikigai explains this beautifully — the intersection of:

what you love

what you’re good at

what the world needs

what you can be paid for

And when those begin to align, work starts to feel less like something you endure and more like something that supports your life.

Because financial wellness isn’t just about managing money.

It’s about how that money is created.

If this is something you’re exploring, I go deeper into this in Right Livelihood: How to Align Your Career With Your Values, because your work and your financial wellbeing are far more connected than most people realize.

Building Emotional Resilience With Money

One of the most overlooked aspects of financial wellbeing isn’t strategy.

It’s emotional resilience.

Because no matter how much you know about money — how to budget, invest, or grow wealth — your ability to make aligned decisions will always be influenced by the state of your nervous system.

And when your body is under stress, your decision-making changes.

There’s research in neuroscience showing that when we’re in a stress response, the brain shifts activity away from the prefrontal cortex — the part responsible for logic, planning, and long-term thinking — and toward the limbic system, which is focused on survival and emotional processing.

Which means in those moments, you’re not thinking clearly.

You’re reacting.

And this is where so many financial patterns are created.

Not because you don’t know what to do…

But because your body doesn’t feel safe enough to do it.

Stress: When Survival Mode Takes Over

Stress is a natural response.

Your body is designed to activate when it perceives a threat — whether that threat is physical, emotional, or even financial. The problem is that in modern life, many of us are experiencing chronic stress, where the body never fully returns to a regulated state.

And when that happens, your baseline becomes survival mode.

Financially, this can show up in subtle but powerful ways:

impulsive spending to relieve pressure

avoiding your finances altogether

difficulty planning long-term

constantly feeling behind, no matter how much you earn

Because when your body is trying to survive, it’s not focused on building wealth.

It’s focused on getting through the moment.

Supporting your financial wellness, then, isn’t just about changing your habits.

It’s about regulating your system.

That can look like small, consistent practices across different areas of your life:

mentally: creating space from constant pressure, reducing unrealistic expectations

emotionally: limiting exposure to toxic environments or relationships

physically: prioritizing sleep, movement, and nourishment

spiritually: engaging in mindfulness, meditation, or practices that create grounding

Even something as simple as taking breaks during the day or creating a more calming environment can begin to shift how you experience money-related stress over time.

Anxiety: When Fear Becomes the Default

Anxiety is often described as persistent worry, but in the body, it’s more than that.

It’s a state of heightened alertness — where your system is constantly scanning for what could go wrong. And when that state becomes chronic, it can make even small financial decisions feel overwhelming.

There’s research in psychology showing that anxiety can impair decision-making by increasing risk sensitivity and reducing confidence, which can lead to overthinking, indecision, or avoidance.

And financially, that might look like:

second-guessing every decision

hesitating to invest or take opportunities

constantly fearing loss, even in stable situations

avoiding looking at your finances altogether

What’s important to understand is that anxiety isn’t something you “fix” through logic alone.

It’s something you work with through regulation and support.

Approaching it holistically can make a significant difference over time:

mentally: using tools like cognitive behavioral therapy to reframe thought patterns

emotionally: creating environments that feel safe and supportive

physically: supporting your body through movement, nutrition, and rest

spiritually: practicing mindfulness to bring yourself back to the present moment

I’ve found that the more you reduce the intensity of the emotional response, the easier it becomes to make grounded financial decisions.

Not perfect decisions.

But clearer ones.

Burnout: When Capacity Is Exceeded

Burnout is what happens when stress and anxiety are left unaddressed for too long.

It’s not just exhaustion.

It’s depletion.

And it doesn’t just affect your energy.

It affects your capacity to care, to think clearly, and to engage with your life — including your finances.

There’s growing research showing that burnout impacts cognitive function, motivation, and decision-making, which can directly affect how people manage money, pursue opportunities, and plan for the future.

Financially, burnout can look like:

overworking without long-term direction

losing motivation to manage money

feeling stuck or unable to move forward

continuing patterns that no longer serve you

And often, it’s tied to overextension.

Doing too much. Carrying too much. Trying to hold everything on your own.

Supporting yourself through burnout isn’t about pushing harder.

It’s about creating space.

That might mean:

taking things off your plate and reprioritizing

learning to set boundaries without guilt

saying no to overcommitment

listening to your body instead of overriding it

allowing yourself rest, even when it feels unfamiliar

For some, it may even mean taking a longer pause — a reset, a sabbatical, or simply a period of recalibration.

Because you can’t build sustainable financial wellness from a depleted state.

Resilience and Financial Wellbeing

What all of this comes back to is resilience.

Not in the sense of pushing through or enduring more…

But in your ability to return to a regulated, grounded state — again and again.

Because when your system feels safe:

your decisions become clearer

your reactions soften

your patterns begin to shift

your relationship with money becomes more stable

And over time, that stability becomes the foundation for everything else.

If you want to explore this deeper, I expand on this in Financial Decision Making: How to Make Smarter Money Choices, Financial Anxiety: How to Stop Money Stress From Controlling Your Life, and Why Hyper-Independence Is Making You Broke and Burnt Out, because emotional resilience isn’t separate from financial wellness.

It’s what makes it sustainable.

The Wealth Wellness Philosophy

At a certain point, everything you’ve been navigating with money — your money mindset, your financial wellbeing, your habits, your emotional patterns, even your income — starts to reveal itself as something more interconnected than it first seemed. What once felt like separate areas to fix or improve begins to feel like part of a larger system, one that isn’t broken, but simply hasn’t been fully understood or integrated yet.

Because financial wellness isn’t one thing you solve in isolation.

It’s something you build over time — and more importantly, something you learn to live inside of.

Why Financial Wellness Needs Integration (Not Just Information)

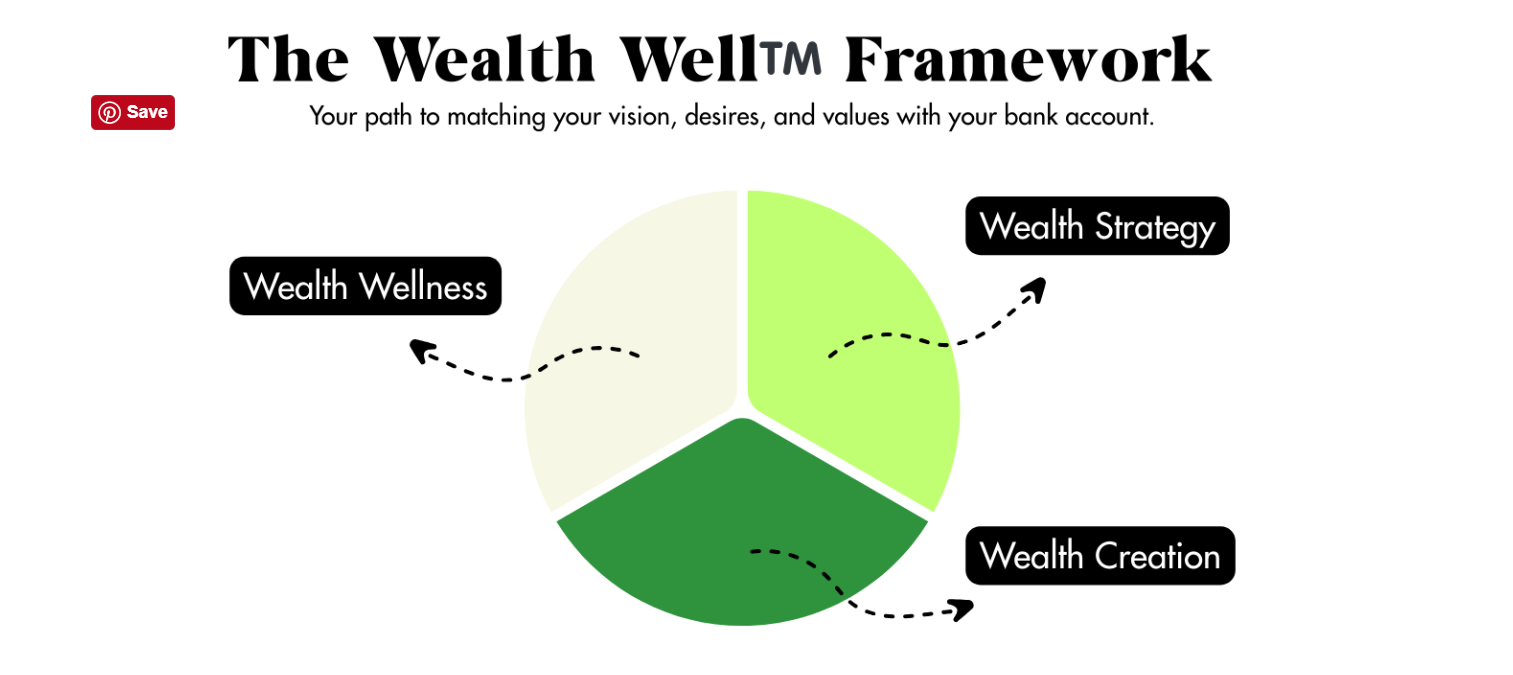

This is what led me to create the Wealth Well™ Framework.

Not as another rigid method or step-by-step system to follow perfectly, but as a way to bring everything together into something that actually makes sense. A way to understand how your relationship with money is shaped not just by what you do, but by how you think, how you feel, and how you live.

For a long time, I felt like I was doing “all the right things,” just not in a way that felt cohesive. I was working on my money mindset in one area, trying to improve my habits in another, thinking about income and growth somewhere else entirely. And even though I was making progress, it often felt fragmented — like I was constantly adjusting one part of my life while another part quietly pulled me back.

What I needed wasn’t more information.

It was integration.

The Three Pillars of the Wealth Well™ Framework

The Wealth Well™ Framework is built on three core pillars — Wealth Wellness, Wealth Strategy, and Wealth Creation — but what makes it different is not just what these pillars are, it’s how they work together. This isn’t a checklist or a linear path where you complete one and move on to the next. It’s a system that evolves with you, where each part continuously influences the others.

At a high level, it looks like this:

Wealth Wellness → your internal foundation

Wealth Strategy → your external structure

Wealth Creation → your expansion and growth

And when one of these is missing, you feel it — even if you can’t immediately explain why.

Wealth Wellness: Your Internal Foundation

Wealth wellness forms the foundation, because your internal relationship with money shapes everything that follows. This is where your emotional safety, your beliefs, your nervous system responses, and your sense of self-trust live. It’s the part of financial wellbeing that most people overlook, especially when they’re focused on increasing income or improving strategy.

But without this foundation, even the best financial plan can feel unstable.

You can be:

earning more than ever

making “smart” financial decisions

doing everything right on paper

…and still feel anxious, disconnected, or uncertain.

Because your system hasn’t caught up yet.

Wealth Strategy: Turning Values Into Structure

Wealth strategy builds on that foundation by giving your money direction. This is where your values begin to take shape in practical ways — how you spend, how you save, how you invest, and how you plan for the future. But this isn’t about forcing yourself into a rigid structure that doesn’t fit your life.

It’s about creating a plan that reflects:

what actually matters to you

how you want your life to feel

what you’re building toward long-term

Because strategy without alignment creates pressure.

But strategy rooted in alignment creates momentum.

Wealth Creation: Expanding What’s Possible

Wealth creation is where expansion happens, but it’s also where a lot of people start — and that’s often why things feel unstable.

This pillar is about increasing income, building wealth, and creating more opportunities. But when it’s pursued without the support of wellness and strategy, it can quickly turn into overworking, overextending, or chasing more without ever feeling satisfied.

More money doesn’t automatically create more ease.

In many cases, it amplifies what’s already there.

When It All Comes Together

What I’ve found is that when these three pillars begin working together, something shifts in a way that’s hard to describe until you feel it for yourself.

Money stops feeling like something you have to control.

And starts feeling like something you can actually work with.

Instead of reacting, you begin responding.

Instead of second-guessing, you begin trusting yourself.

Instead of chasing, you begin building.

And your financial wellness becomes something you experience — not just something you’re trying to achieve.

If you want to go deeper into how to apply this in your own life, I expand on this in The Wealth Wellness Framework: 3 Principles for Building Abundance and How to Do a Life Audit to Transform Your Life and Money, where you can begin to map out how each of these pillars shows up for you personally.

Because at the end of the day, this isn’t about becoming someone different.

It’s about becoming more aligned with who you already are — and building a relationship with money that actually supports that.

FAQ: Financial Wellbeing, Money Mindset & Wealth

What is financial wellbeing?

Financial wellbeing is your emotional, mental, and practical relationship with money. It’s not just about how much you earn or save — it’s about how safe, confident, and supported you feel when managing, spending, and growing your money. True financial wellbeing means your money aligns with your life, not just your numbers.

What is the difference between financial wellbeing and financial wellness?

Financial wellness often refers to your overall financial health — things like budgeting, saving, and managing debt. Financial wellbeing goes deeper. It includes your emotional experience with money, your money mindset, and how you feel in relationship to your finances on a daily basis.

How does money mindset affect financial wellness?

Your money mindset shapes every financial decision you make. The beliefs you carry, whether conscious or subconscious, influence how you earn, spend, save, and grow money. If your mindset is rooted in fear, scarcity, or self-doubt, it can create patterns that limit your financial well-being, even if you’re earning well.

What does it mean to have a healthy relationship with money?

A healthy relationship with money means you can engage with it without constant stress, guilt, or avoidance. It means making financial decisions from clarity instead of fear, and feeling grounded, confident, and intentional in how you use and manage your money.

Is money manifestation real or just a mindset?

Money manifestation is most effective when it’s grounded in both mindset and action. It’s not about thinking positively and waiting — it’s about believing in what’s possible for you, aligning your behavior with that belief, and consistently taking action over time.

What is money energy?

Money energy refers to the emotional tone of your relationship with money. It’s how you feel when you earn, spend, save, or think about money. Those feelings influence your behaviors, which is why your emotional relationship with money plays such a powerful role in your financial wellbeing.

How can I improve my financial well-being?

Improving your financial wellbeing starts with awareness. From there, you can begin to shift your relationship with money through both internal and practical changes, such as:

identifying and rewriting limiting money beliefs

reducing financial stress and creating emotional safety

practicing intentional, values-based spending

aligning your income and career with your values

building habits that support long-term financial wellness

Over time, these shifts create a more grounded, confident, and sustainable relationship with money.

If you’d like to keep journeying together…

→ Start Here: free tools and reflections to help you feel grounded, clear, and more confident with your money.

→Work With Me: private coaching, strategy sessions, and programs designed to help you build wealth that feels aligned, stable, and sustainable.

→ Subscribe to the Channel: If this resonated, come hang out with me on YouTube where I break this down in real life — the habits, the mindset shifts, and what this actually looks like day-to-day.

→ Or Join My Email List: This is where I share deeper insights, behind-the-scenes thoughts, and the kind of conversations we don’t always have publicly.